2020 Q3 Commentary

By Jason Lesh, Managing Principal

Election day is finally here. And regardless of outcome, today feels like one of the final chapters in what has proven to be one of the crazier years in modern history. To say we are living through strange times is a gross understatement. Wildfires throughout the west. Global pandemic. Mass unemployment and an upended business environment. Huge government financial intervention. Social unrest. Quickly changing landscape on nearly all fronts from healthcare to education to shopping. 2020 has at times been exhausting, polarizing and can feel like we have lost control.

But today is a reminder of our individual responsibility and a choice that speaks to the long-term direction we each want for our country. A decision rooted in our personal ideals and values. We will save you from our personal political musings, but 2020 has certainly made us pause and take stock of many things. At the end of the day, it is good to challenge our thinking. To put our mental models and frameworks to the test. To delve deeper and commit to being life-long learners. To revisit what it is we said we stand for and how we choose to uphold those convictions. In that respect, we are grateful for the opportunities that 2020 has afforded us so far, both personally and professionally.

For all of the noise and craziness that the past 10 months have served up, we are still laser focused on making long-term investment decisions. As we have talked about incessantly over the years, we are unabashedly value investors. At times, such a strategy can feel boring. At others, it can feel scary. Much to the chagrin of the young talking heads, value investing is not dead and it is good to remember that historical data indicates value investing outperforms the general market over the long-haul. Especially in times like these.

In the following pages, Nick revisits the rollercoaster of the year and some surprising trends. There are definitely reasons that give us pause on being risk-averse and blindly buying growth. But we are also extremely excited about the portfolios and our individual holdings. In the midst of a chaotic year, we see reasons to be very optimistic. And over the coming decade, we look forward to seeing the seeds of our investment decisions continue to flourish.

I hope this note finds you well and know of our continued well wishes.

Warmest regards,

“Prospective returns on everything are about the lowest they have ever been.”

Imagine it is October of last year (2019) and I told you that we would be in the middle of a global pandemic. Firstly, I’m sure we would all hope our family and loved ones are healthy. Then I would surmise you would begin to ask a series of questions around what life looks like in a pandemic. Lots of uncertainty for sure.

On the economic front, we have had $5T of fiscal and monetary stimulus following the initial $2T shock to the US economy. We suffered a massive loss of jobs with only 50% having been recouped thus far. Delinquencies on federally backed “FHA” mortgages have soared with 1 in 6 borrowers having missed their mortgage payments. Former Treasury Secretary Larry Summers authored a study estimating the total economic impact to be $16T over the course of the pandemic.

The profits of the largest US companies as a group have fallen to 2011 levels which is equal to the amount of profits from 2006. No one alive could comprehend how this would compare to anything but the worst economic environment in our history. And it is. But…

With all that, how would you expect financial markets to have responded?

You’d expect interest rates to have fallen to zero…and they have.

You’d expect corporate bankruptcies to have spiked…and they have (although not nearly as much as expected).

You’d expect the real estate market to have slowed…and it has on the commercial side, although not residential.

You’d expect the stock market to have cratered…que the abrupt scratching record noise! • Wait the stock market is up? How could this be?

With all the stimulus (supplemental unemployment and stimulus checks) personal income has risen 12%, despite the depression like conditions. It is estimated that a significant amount of this “disposable income” has gone into the stock market. Below you can see the actual benefits to those unemployed have been hugely beneficial, increasing their cash balances and spending throughout this crises.

We remain cautiously optimistic on the economic front, as long as there is a willingness to continue fiscal stimulus. I suspect it will come no later than February. It is possible the market forces congress to pass something sooner, but we are going to find out just how strong the economy is without the support.

Market Bubble

The allure of growth in a zero interest rate environment is very strong and benefits those companies that have a great story to tell. For example, if you bought the stock of every company that was losing money with $1B or more of market value at the end of 2019, you would have gained 65% so far this year. These companies have a story of revenue growth – no matter the cost. Ignoring cost doesn’t make for a prudent investment strategy.

This has ushered in the second US stock market bubble of my lifetime. According to market historian Charles Kindleberger, there are a few things common in all bubbles, whether it be the Tulip bubble, South Sea bubble, Mississippi Co, Railway bubble, Roaring ‘20s, Nifty Fifty of the ‘70s, Junk Bond bubble of the ‘80s, .Com bubble, Real Estate bubble, and the current (yet to be named) bubble. Note that several valuation measures exceed that of 1999/2000, including enterprise value divided by earnings before interest and taxes.

These commonalities in all bubbles include:

Disruptive technology encouraging new investment.

A boom narrative along with financial innovation bringing about leveraged returns.

A speculative euphoria phase brought on by a “nouveau riche” class of investors.

Crisis after a fall in prices causes forced selling among leveraged speculators.

As long as investors maintain their faith in a new era and ignore dissonant information, then stocks will continue to rise. In the short run, a rising market serves to cover up weaknesses in the economy. Consumers spend their stock market gains and ignore their rising debts, companies issue new shares or bonds to purchase other companies or finance capital expenditure, as the economy prospers. In this way the new era analysis becomes something of a self-fulfilling prophecy.

On a side note, I don’t remember many investors in hindsight saying they wished they would have had more exposure to the tech sector during the 1999 run. We shall see if this time is different. Most people realize that it’s nearly impossible to sell at the top unless you already believed that there was a bubble and by the very nature of that thought process it would preclude everyone but those most open to speculation from participating in the first place.

Is it all doom and gloom? No. We are actually excited about owning certain things right now.

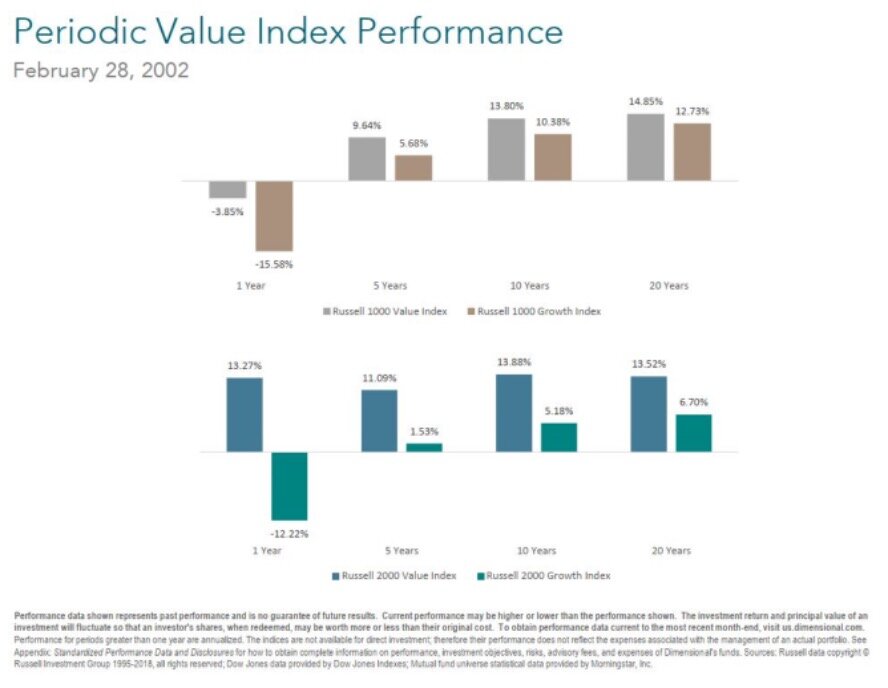

It’s important to remember that just because there is a certain segment of the market unduly influencing investors, doesn’t mean that we can’t achieve a respectable return over time. In fact, the years after the 1999/2000 bubble showed a real dichotomy in stock prices. Consider that for the five years ending 12/31/1999 value stocks had underperformed technology related growth stocks by nearly 9.5% per year!

It took a mere 14 months for the outperformance to completely reverse in favor of value stocks by February of 2002.

The most expensive stocks languished for years, despite terrific business results from many of them (think Microsoft, Amazon, Cisco, etc). This downward pressure caused the S&P 500 index to underperform for years afterward. In the meantime, the stock prices of many of the previously “boring” and overlooked areas (emerging markets, commodities and “main street” sectors of the economy, value stocks) performed very, very well. I expect that this time we will see something similar over the next 10 years. Note that the outperformance among the small stocks of the Russell 2000 was even more pronounced.

The equity holdings that we are invested in have underperformed for the most part this year. As a result of this underperformance and the absolute cheapness of these investments, we may have the best setup we have seen since late 2015. We are very convicted in the things we currently hold.

With the overall cost of Covid, we expect that inflation will take hold eventually. We remain a bit cautious on the whole, and are not afraid to be more aggressive as the environment shifts from one of deflation to inflation. We thank you for your continued support as we continue to progress through this unique environment together. There is no doubt that things will be different as we emerge out the other side of the pandemic.

“Perhaps more than anything the bubble economy illustrates the danger that arises when investors believe that market risk is shouldered by the government rather than by themselves. Throughout the late 1980s, sceptics were told that the Japanese government would not allow share prices to fall and that Japanese banks and brokerages were ‘too big to fail.’ When the bubble collapsed a few years later this belief was revealed for what it was — an ignis fatuus that led banks [investors] to their ruin.”