Corporate profits are at an all time high as compared to GDP. This week we talk about the likely reasons why and look forward to what this means to future earnings and possible changes that may lie ahead.

STRATEGY & WISDOM

Rarely is our attention captured by a short term chart, however, in the following from Bloomberg it illustrates the significant appreciation in long term Treasury bonds since the beginning of the year. Not only was this unanticipated, but the opposite was the prediction from most experts. Validity of predictions aside, it does beg the question what should be done with positions that are long on bonds? Listen to the following discussion and hear what Pilot's Portfolio Manager, Nick Fisher, has to say.

If valuations actually matter anymore, and the U.S. is in fact overvalued - then what do we want to buy? This week we look at cyclically adjusted price-to-earnings ratios (CAPE) of other foreign markets and the returns that they generate. Fittingly, we also discuss the difference between risk, volatility, and the permanent loss of capital.

Cov-lite lending and commercial loans have grown quite a bit in the last couple of years. This week, we discuss what covenant light commercial loans are, how they are made, and how the risk is mitigated by lenders. All of this of course informs our risk vs. return assumptions and the evolution of our fixed income allocations.

Successful business owners and leaders recognize that leadership effectiveness directly impacts employee commitment, customer retention, organizational performance and ultimately, profitability. It's the "secret sauce" to fulfilling a vision. Join us for Part 3, Navigating Conflict and Fostering a Collaborative Culture!

arguing

When it comes to business partnerships, finding and maintaining a productive partnership can be as challenging as a marriage. Perhaps even more so given that many business partnerships are nothing more than shotgun marriages; the result of a courtship based solely on the financial merits and not much more. I liken this to marrying someone based solely on how attractive you predict the children will be, without regard to whether the two of you will be able to stay together. The refrain, “Failure is life’s greatest teacher,” speaks directly to my experience and in this regard, I have earned a PhD, having suffered through two failed business partnerships before figuring out how to enter my most recent one with the best opportunity for success. Additionally, through my advisory work I have observed many partnerships in action, brought in to assist when the partnership is going off the rails. It is usually then when most partners begin to realize the complexities of the partnership, far beyond the dollar signs they had floating in their eyes when they first came together.

When I ask partners that are experiencing conflict and potentially on the brink of collapse, “what would you have done differently?” I almost always hear the same two responses; “I would have asked a lot more questions,” and, “I would have taken more time.” And this is the crux of the issue—most people do not take enough time to truly vet the potential partnership for issues that will derail it. This happens most often because there is the rush of a deal or market timing driving the urgency, and as partners in the midst of conflict will testify, no partnership, no matter how lucrative the opportunity may appear, is worth the pain and suffering caused from premature and ill-prepared agreements.

The reality is, attempting to repair a partnership that is deep in conflict and has not done the preparatory work to set it up for success is much like trying to unscramble the omelet. Not that it can’t be done, but on a scale of difficulty, it is much larger than I can do justice here and suffice to say, often the cure kills the patient. Rather, the best opportunity for success is if you are in the early stages of formation. Following are some key steps I recommend to ensure you enter the partnership with eyes wide open and prepared for the work it will take to achieve success:

Slow down – As I’ve already stated, there is no deal so important as to overcome the poor planning of a rushed deal.

Look for a reason to say no – This sounds contrary to what you’d want, but the mindset of no is necessary to force the hard questions and rationale of, “why the partnership?” Be clear about this and force yourself to write it down. Actually, there is a whole lot more here than I have the space to write, but suffice to say it is adequately covered in David Gage’s The Partnership Charter.

Clarify roles – One of the key issues I see is that partners don’t clarify their roles “in the business” as employees, versus “on the business” as partners. There is a key distinction and clarifying when and how these roles are defined can often be the difference maker between success and failure.

Go deep on values – If they even go through the effort of defining values at all, most people short the process. It is not enough to know that all agree that integrity is a value, for example. You need to go deep, defining what behaviors define integrity, so everyone is clear what it is, and what it is not.

Define how to exit – Most partner agreements avoid this step, however force the conversation around how to value the business, or in the least, who would do the valuation, and agree on what those steps would are ahead of time.

The reality is there is no guarantee, however as the saying also goes, success favors the prepared. With patience and effort you will avoid the proverbial Rodney King moment when you are exclaiming to everyone, “Can’t we all get along?”

You can find a chart that will tell you whatever you want it to: here are a couple that we will do very little with. Pascal is famous for the saying, "All of man’s misfortune comes from one thing, which is not knowing how to sit quietly in a room." And so while we are aware of some past trends, activity for activities sake is dangerous and stupid in our mind. We will wait for a bit of volatility. And be entertained along the way.

With the Fed meeting later this week and the prospect of continued tapering of asset purchases, it is a good time to revisit the theory behind Quantitative Easing. In this extended discussion, we look at the impact of QE, the hope of what it will induce, and how we are planning for the uncertainty. We refer back to our 2013 Q3 Commentary and the capital markets line in the proverbial quest of answering the question of "what do we want to own?"

We have written in last quarter’s report that we should expect lower annual market returns than what were achieved in the previous 4 years. The reason for this has less to do with a change in the vigor, (or lack thereof) with which our economy grows and more to do with the price paid for assets in today’s environment. To explain let’s first review the rationale of any capital allocation decision and finish with discussing the significance of volatility and the need for unconventional thinking. The basis of any capital allocation decision has not changed since Aesop’s truism in 600 B.C., “a bird in the hand is worth two in the bush.” Warren Buffett, in his letter to shareholders in 2000, added three questions to this enduring axiom: 1) How certain are you that there are indeed birds in the bush? 2) When will they emerge and how many will there be? 3) What is the risk-free interest rate [how would your bird in hand grow without taking any risk]? Of course, in Buffett’s example birds are dollars and a bush is any capital outlay or investment. If you can answer these three questions with certainty, than you will know the maximum value of the bush (investment) and the maximum number of birds (dollars) that should be offered for it.

ocYR3Us

Of the many demands growth brings to a business, the aspect most owners are unprepared for is the demand on the financial infrastructure of the business to support the business growth. This is especially the case for entrepreneurs and small businesses where owners face multiple demands such as customer management, deploying strategic initiatives and dealing with an increasingly complex world of labor law and regulatory compliance. Feeling the pain of being pulled in too many directions, owners often attempt to address the financial demands by seeking to hire a CFO, believing that their problems will be solved.

We observe this frequently and it underscores how misguided many are as to what a CFO brings to the table. Often times, CFO’s are hired for the cache value; the perception of having a CFO in the business, rather than for the deeper knowledge of what it takes to leverage the value of a CFO, let alone afford one.

For an expert’s opinion on this, I asked Wayne Marschall, Vice President and Chief Financial Officer of The Stoller Group to weigh in on this topic. Not only has Wayne served in multiple executive leadership roles as a CFO for both large and small companies, Wayne is also serving as the 2014 Portland Chapter President for Financial Executives International (www.financialexecutives.org), a financial industry association focused on the professional development of financial executives.

“The inflection point for a business being able to leverage the value a CFO brings to the table is around $50 million [in revenues],” Marschall explained. “That is when a business begins to transition from a controller or bookkeeper mentality, which is primarily looking in the rear view mirror, to one that is forwardlooking and leverages the business intelligence in the strategy and planning. A CFO can bring the sophistication and nuance to these processes to scale the business in an effective way.”

Wayne’s points are well taken. Does it mean, however, that the services of a CFO are out of reach for small businesses that have not reached that inflection point? No. There are many qualified contract CFO’s that provide excellent guidance to small organizations on a contract basis. The clarification that we will make here is that often the CFO-for-hire is no more than an accountant turned contract CFO, providing just good accounting practices. While these services may be needed, they are not offering the value of a true CFO. In order to prepare the business for leveraging the value and investment of a CFO, (full time or contract) the following should be in place and are what Wayne refers to as the building blocks of an effective financial infrastructure:

1. Solid accounting processes – Accounting software and processes that generate financial reporting that has integrity and provides the owner with business intelligence, i.e. the ability to drill down at a line item level and identify what the specific expense, income or balance sheet item it is and what drove the number. Included in this is good history so that the numbers tell a story over time of what the business has been doing.

2. Competent talent – For a small growing business, this can often be the most challenging aspect of building a financial team. Legacy employees often do not have the skill sets necessary to meet the needs of a scaling business. Whether through training and development or new personnel; however it is accomplished, talent is required to drive the systems.

3. A planning and forecasting process – This is a key pivot point for the business in beginning to look forward in a proactive way rather than continuing to react and is the key difference between the activities of an accountant and a CFO. Further, ensuring the budgeting and business planning is aligned with the business strategy creates the efficiency in the systems needed such that the intelligence can be deployed nimbly. This along with sound business strategy creates a holistic business process that is a force to be reckoned with, no matter the market.

"The key question that needs to be asked,” Marschall reiterated, “is do I have the people, processes and tools to get me there?” The benefits of a CFO are best utilized when these building blocks are in place and functioning. Otherwise the business will not leverage the talents and expense of bringing a CFO to the table.

Earning estimates at the end of Q1 are much different than they were back in January. This week we explore how they have evolved over the last three months. The goal is to provide context for the proverbial headlines of "Company X beat estimates by $0.05 per share" that we are sure to hear.

Finding your business's sweet spot can be as elusive as a snow leopard or an albino gorilla. Like most leaders, you're on a quest to move your company towards growth and greater success. But how do you best focus your efforts to actually make that happen? In this webinar you'll be challenged to rethink conventional business wisdom and achieve excellence by aligning your passions and talents with market opportunities.

The rising tide does not raise all boats. In this week's conversation, Nick Fisher addresses the rotation from last year's losers into Q1's all stars.

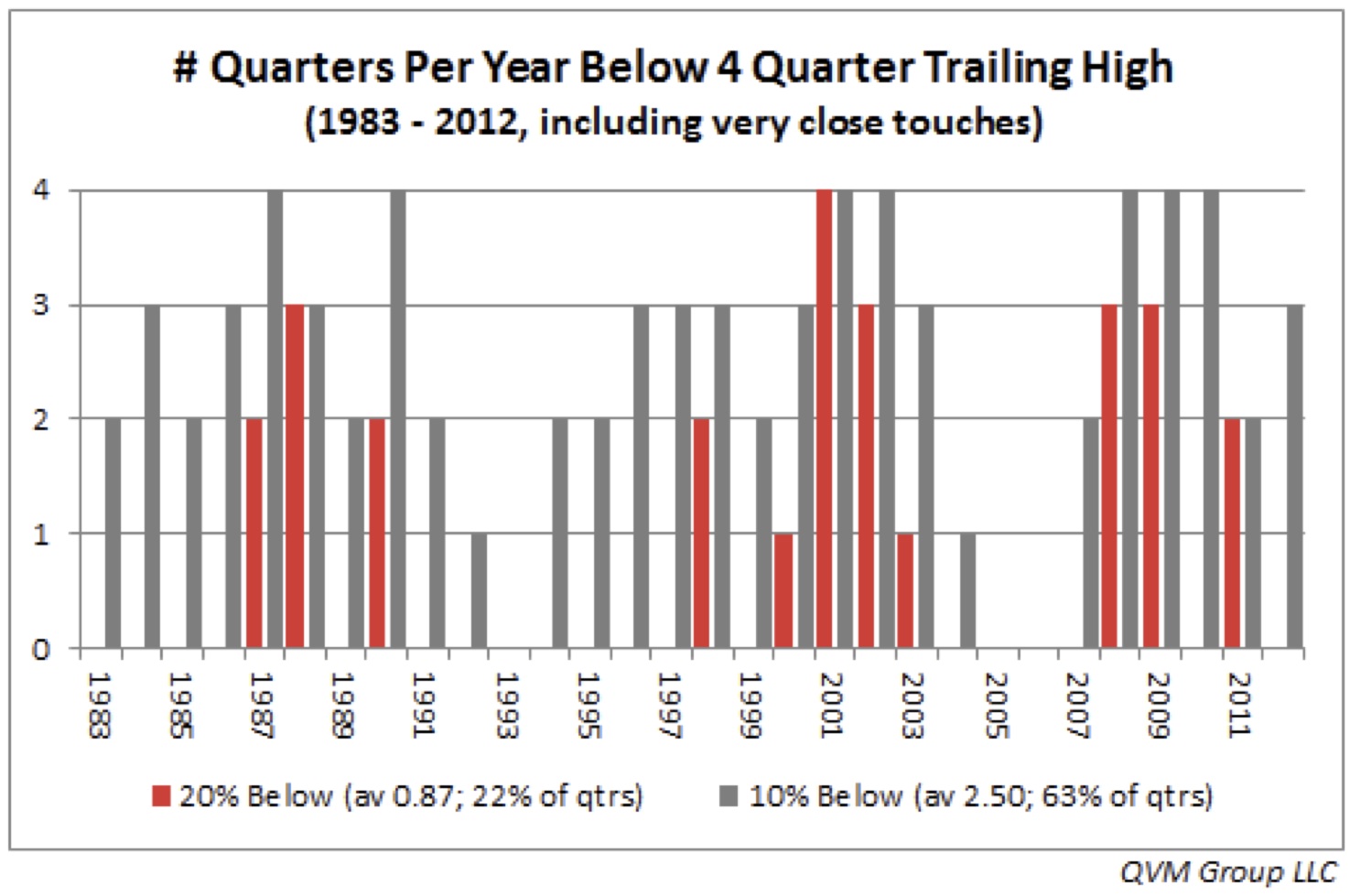

In this week's Chart of the Week, we discuss increased volatility, how often it occurs, and what it means to investors.

In 2000, the market’s PE ratio was nearly double that of 2014. Ironically, there are less companies for sale today at valuations we are comfortable with. Learn more in this Chart of the Week with Pilot's portfolio manager, Nick Fisher.

Bubbles have predictable patterns: human emotions can drive asset prices to irrational levels. Understanding this can hopefully help us avoid following the lemmings off a cliff.

Interest rates could be quite volatile as investors digest the Treasury's need to refinance the short term maturities of our national debt.

“The less prudence with which others conduct their affairs, the more prudence we must use in conducting our own.”

-- Howard Marks’ favorite quote

As a portfolio manager, I have two jobs: 1) Define the playing field by understanding risk and 2) Once the playing field is defined, invest in opportunities that offer our clients the best risk adjusted return in order to achieve their goals. Last quarter we discussed our probabilistic approach in defining the playing field and understanding the dynamic of the risk/return tradeoff. This quarter I will update you on our thoughts on risk and share some thoughts on portfolio construction in light of these risks and uncertainty.

Unlike our parent’s generation, it is a virtual given that most will face several career transitions in our lifetime. I entered the workforce soon after college in 1986 and have experienced four key career transitions. Knowing these transitions are the norm rather than the exception these days, there was a process I learned after my second transition that proved to be valuable in ensuring I was making good decisions for me and my family-a Council of Advisors. While well known in the business world in the form of a Board of Directors or Board of Advisors, the function is similar-where ideas, inspirations and dreams can be tested and then be held accountable for action. Too often, career decisions are made in haste or in response to short term opportunities and needs, ignoring the long term. The reality is that no matter how good the jobs and opportunities seem to be, a successful career is not built on short term success, but rather over the long haul and more so when continually held against a broader objective of where one is aiming. Whether you find yourself at a transition point in your career, or if you feel your current direction is a dead end and are uncertain which way to go, the following steps can help get the process going:

1. Begin with Why - It is a given when people ask for my advice on career planning, that I will ask them at some point, why? Why that career? To further challenge them, I will clarify that it cannot be about the fortune or fame. If you have not defined your Why, then begin here. A well defined purpose reframes a career trajectory and brings meaningful action to your goals (check out Simon Sinek’s Tek Talk on How Great Leaders Inspire Action. He also has an online course on defining your purpose atwww.startwithwhy.com).

2. Define your council - Whom you invite onto your team may be as important as what you talk about. Your circle of friends is a great place to start, but consider the following qualities when determining whom you will ask:

A. Humility - Simply put, can they put your interests above theirs? Someone who demonstrates humility over ego will keep your interests at the forefront and not feel challenged to “compete” with your desires.

B. Mix it up - The more diversity in perspectives you can bring together, the better. A variety of backgrounds, gender and generation will ensure you are capturing as broad a perspective as possible.

C. Brutal honesty - You must be willing to be held to the often-harsh light of reality. While difficult enough to hear it, it is even more difficult to offer it up to others. Those that are grounded in who they are will be willing to offer the brutal truth.

3. Get a facilitator - Even in the best of circumstances with the right people at the table and a clearly defined purpose, attempting to manage the conversations on your own will create results that are underwhelming and frustrating. A good place to start looking for a facilitator is within the council itself, especially if any of them have experience. Career coaches can also be a good source for facilitation as well. However you find it, make sure you have someone else in the process beside yourself to direct the conversations.

4. Start meeting - Avoid the desire to get things perfect before you meet. Perfectionism is often a stalling tactic. The sooner you start the conversations, the energy around the career planning will be apparent. Frequency for the meetings is somewhat determined by your particular situation, however I would suggest as a starting point to schedule your first couple of meetings within a two months of each other to get continuity and lay the groundwork. Once you begin identifying longer-term objectives, an annual check-in is suitable. You can also call an ad-hoc meeting as situations arise in opportunities or unexpected events and need feedback in the short term.

Lastly, keep in mind that career planning is a marathon, not a sprint. Small, meaningful steps are much more valuable that energetic starts that are not sustained. But more than anything, take action and sooner or later you will learn which direction is right for you.

Screen Shot 2013-12-30 at 11.08.20 AM

While I am an advocate of an annual planning process, there is often a common mistake made with strategic initiatives-they focus too often on the programs and ignore the most important strategy of all-ensuring it has the foundational elements of what builds an enduring business.

Camping with my dad when I was young provided me the framework to understand this. The campsites we stayed at rarely had level surfaces and demonstrating with a portable campstool, my dad showed me how a three-legged stool always finds its level. Sure enough, as I tested the campstool I found that no matter how uneven the ground, it did not rock when I sat on it. The analogy of the three-legged stool has stayed with me over the years and having since experienced the turbulent and often uneven landscape of the free market in the aim of building an enduring business, I have found that it applies here as well.

There are three principles that are crucial to enduring businesses, that when well understood and internalized by the organization, will allow the business to withstand any economic climate. They are as follows:

Purpose - A well-understood and communicated explanation of why the business exists (which by the way, is not about the money), and more important, why it matters, both to the business owner and to the customer. One could even argue that the latter is more important than the former. To underscore this, consider the following: Koch Industries built the largest privately held business in America based on the principle that understanding what creates the greatest value for their customers is the most important thing. The first and most important element of its MBM® (Market Based Management) Framework is, "where and how...the organization can create the most long-term value for customers and society." If it is good enough for Koch in building a $100B+ business, it is good enough to work in our businesses as well. Notice the emphasis on the long-term...something that often is lost in the noise of deal making.

Competence - The business must be great at what it does, and by my definition is the combination of talent, learned skills, and scar tissue from surviving a fire walk-leading the organization through a brush with mortality. To gain competence in your business, you must first be willing to sacrifice for it, be skilled enough to run faster and smarter than the competition, and then have the good fortune of having lived through the fire walk before you truly acquire competence.

Business model - This one is the most fickle of the three. While the first two can endure for the life of a business, the business model may not. Some stand the test of time, many don't. A good model one year can be extinct the next, and often for reasons that are beyond the control of the entrepreneur.

To illustrate this point, I'll draw on an example of a good friend who had opened a retail PC business in his rural hometown about ten years ago. As a savvy engineer and self-proclaimed technology geek, he enjoyed helping people make technology decisions for their personal and business use. The small town he lived in did not have a local PC store or a reliable resource for setting up and troubleshooting home and small business networks. Thus, he opened a retail outlet for both and was soon enjoying a growing patronage. Not long after, a greeting card shop opened next door and he watched curiously to see how long the business would last. As his business continued to build, he began experiencing all the implications of a retail business; warranty returns, damaged product and an occasional fussy customer, the last of which, by his own admission, he was wholly unprepared.

All of this put pressure on the slim operating margins of the PC's that also depreciated quickly on the shelf due to the short lifecycle of the rapidly changing PC technology. Adding to this the hassles of hiring, firing and managing employees, he began to question whether he had it in him to keep it going. As he had also shared, the business was never intended to be end-all, but rather a means to provide a lifestyle he could enjoy while the operation ran largely on its own momentum. It was about that time that he noticed the traffic next door had grown to a steady stream. Staring at his own inventory of expensive computers that were already being discounted, he experienced the proverbial epiphany by 2x4-he didn't have the right business model.

Unlike his PC and service products that were expensive, complex, and prone to failures or repeated service calls, the card shop next door had inexpensive product, virtually non-existent failures, higher margin and long shelf life.

"I finally had to admit that no matter how well the business was managed," he said soberly, "if I don't have the right model, I'll never get to where I want to go. And I didn't have it."

As he realized, defining the right strategy for your business must include an assessment of your business model, under harsh light of what Jim Collins (Built to Last, Good to Great) calls, "the brutal facts of reality." If you do not have the right business model, you must come to terms with that. No amount of wishing or good intentions, or IT initiatives will change the reality of that situation. My friend sold his business within six months of realizing what was missing in his strategy.

Best understood by performing a Strategic Alignment Assessment, there are some questions, however, that can be answered to begin understanding whether your business has these three foundational elements: 1) Do you or your organization understand what it is passionate about? Do your customers know it? Why does it matter? Again, this is not about how much money the business is making. 2) Is the business good at what it does? Has it defined its Circle of Excellence? Has it learned to say no, to focus on what it can say yes to? Has it experienced a do-or-die moment and lived to tell about it? 3) Does the business accelerate with scaling? Are the margins defendable? What is the strength of its position between the supply and demand? Does it have high capital requirements? A Porter's Five Forces analysis can also be very helpful here.

However you or your organization arrives there, the combination of the three foundational principles will ensure you are building an enduring business to stand the test of time.

We share some thoughts about what we believe on our Pilot’s Log and Navigating Markets including words of wisdom inspired by the greats, periodic updates about current markets and timely seasonal reflections.

2233 NE 45th Avenue

Portland, Oregon 97213

Office: 503-847-9723